In the history of the world, perhaps no entity exposes humanity’s split personality greater than money. We love it in our possession, yet we hate its grip on us. We want to acquire as much as possible yet romanticize a life without it. We believe more of it will make us happier, while understanding that the single-minded pursuit of it will bring us misery. Yet, undoubtedly, it is an essential facet of life and understanding how to develop a healthy relationship with it is crucial.

I discovered Morgan Housel and his book, The Psychology of Money, while listening to the Tim Ferris Show. Housel is a partner at Collaborative Fund, an investment firm, where he also writes for their blog. He started his career as a columnist at The Motley Fool, an investing website, and The Wall Street Journal. During his conversation with Ferriss, I was impressed that Housel was not touting a snake-oil prescription of how to get rich. He did not claim to have a secret formula or promote specific stocks.

Instead, he spoke about using a flexible set of principles depending on his goals, how he tries to do what is best for his family’s independence, and why he plays the long game of wealth versus trying to get rich quick. All of which sounded reasonable and logical and not at all sensational.

Housel also emphasized a couple of points that sold me on his book because they aligned with my personal philosophy with money. First, he emphasized that the greatest and most powerful benefit money provides is the potential for independence. The only limited resource we have is time and, if utilized properly, money lets us have our time back to use as we want. Having our autonomy with time is more important than any material good we can purchase.

Second, Housel brought up the incredible point that 99% of Warren Buffett’s wealth was accumulated after the age of 50 and 97% after the age of 65. The only reason Buffett is so wealthy is that he stayed in the game long enough to let his wealth compound. If Buffett had retired at age 50 with his hundreds of millions of dollars, we might have never heard of him. But because he worked for another 30 years, because of his longevity, we now consider him to be one of the greatest investors of all time and one of the richest men in the world.

I decided to read The Psychology of Money to further understand Housel’s perspective. It reminded me of some ideas, taught me others, and made me rethink some of my misconceptions. The New York Times recently reported that many Millennials and Gen Z’ers are forgoing saving for retirement due to their perception of the world’s “doom and gloom” and their desire to enjoy the moment instead. Further, a recent study at Fidelity on the state of retirement planning found that 45% of young people “don’t see a point in saving until things return to normal.” These articles only impressed upon me the importance of financial literacy and why reading this book is important, even if you do not agree with the entire premise. Here are my seven major takeaways:

Learn the Meaning of “Enough”

Humans are inherently irrational beings, designed to constantly seek out validation, rewards, and other forms of gratification. We cannot help but compare ourselves to our friends, neighbors, and, especially, to the masses on social media. If we are not careful, we might find ourselves persistently moving our financial goalposts, always striving for more and never finding satisfaction. Housel touts the importance of learning to say “enough” once your important needs (including a safety net) are met and your family is comfortable. Time spent with loved ones is more valuable than time spent at the office, scratching and clawing for diminishing returns.

Understand the Difference Between Being Rich and Wealthy

Being rich is a state of one’s current income, which may or may not last. It is overt and materialistic. Being wealthy is hidden and unassuming. While some people may be both rich and wealthy, many people maintain the appearance of being rich despite living on the edge of bankruptcy. And yet, despite not having a high income, one can still be wealthy if financially prudent decisions are made. Wealth is income not spent; it is options, assets, or flexible choices that one possesses that can be used to buy more things later than one can right now. The very definition of wealth is not spending the money that you have but instead maintaining possession of it.

Housel writes,

“Exercise is being rich. You think ‘I did the work and I now deserve to treat myself to a big meal.’ Wealth is turning down that treat meal and actually burning net calories. It’s hard, and requires self-control. But it creates a gap between what you could do and what you choose to do that accrues to you over time.”

Power Laws Make Most of The Difference

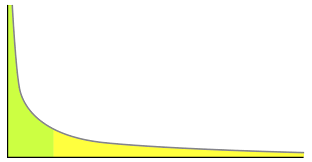

Meaningful differences in the world are the result of power laws, where small changes in input lead to greater relative changes in output, regardless of the initial values.

To the left (in green) are the entities that seemingly dominate all the resources. To the right (in yellow) is the long tail, a property of power law graphs. A classic example is the Pareto principle, which is a business maxim that states 80% of the results are due to 20% of the effort. While the percentages might differ depending on the context, the main idea is that a small number of influential components lead to a majority of the results.

When discussing venture capital investing, Housel illustrates this point by stating that out of 21,000 venture financings from 2004 to 2014, 65% lost money, 2.5% made 10 to 20 times the initial investment, 1% made greater than 20 times, and only 0.5% (100 companies) made 50 times the initial investment. And it was these latter 100 companies where most of the industry’s returns came from.

Housel further elaborates, connecting the idea of power laws to fortune in your life:

“Over the course of your lifetime as an investor the decisions that you make today or tomorrow or next week will not matter nearly as much as what you do during the small number of days — likely 1% of the time or less — when everyone else around you is going crazy.”

In other words, understanding where and when to invest your time and effort for maximum gains is invaluable.

Savings Rate is More Important than Investing

Like many young investors, I have been enamored by the idea of compounding and letting my money “work” for me. But Housel brings up a valuable point that real wealth is made more by your savings rate, because that is something directly in your control. Investing is powerful because by slowly contributing funds to an account, you can watch your wealth compound over time. However, as we can see in today’s financial climate, this is sometimes wildly unpredictable depending on the news of the world. Gains built up over years can be wiped out in weeks. But choosing how much of your income to save in a bank versus spending it is entirely in your control. The money in a bank will not compound like if it was invested, but it is a valuable safety net and source of flexibility that is easily accessible.

Leave Room for Error

I find myself trusting this book because Housel offers reasonable, measured advice. He does not recommend going pedal to the metal with risk in an effort to maximize gains. He emphasizes that becoming wealthy requires a different attitude than staying wealthy. Once you are on the path to wealth, you must be careful not to squander it. To that end, he recommends having a margin of safety in your financial plan. Give yourself enough leeway to occasionally make a mistake, which will inevitably happen, without becoming wiped out by an investment decision.

Housel writes,

“The trick when dealing with failure is arranging your financial life in a way that a bad investment here and a missed financial goal there won’t wipe you out so you can keep playing until the odds fall in your favor.”

In other words, stay frugal, flexible, and focused.

Anticipate that You and Your Goals Will Change

Three to five years ago, I could not have imagined where I would be today or how my goals have changed. Different opportunities, circumstances, and people have slowly and, on occasion, dramatically transformed me and I anticipate I will continue to evolve for the rest of my life. It does not make sense to stay so rigid in your beliefs that you miss an unexpected chance to try something different that could improve your life. Perhaps that is moving to a new city or making a new business partner or letting yourself fall in love. Life is unpredictable and the biggest changes are the ones that will not see coming. Stay open to the good or bad that comes so that you can adapt accordingly.

Have Humility

As with most things in life, the best results comes when we are humble. Do not get carried away in status games or keeping up with the Joneses. Stay flexible and open in your thought process. Maintain room for error for when things inevitably go against you. Do not let yourself become coldly focused on profits and lose sight of the inefficient but joyful parts of life. Recognize that life is fragile and things can be taken away from you quickly and without warning. While our relationship with money is important, it does not compare to how we relate with our family, friends, and community. Let’s be careful not to take them for granted.

Thank you for reading.

Interested in learning more? You can support me by:

- Purchasing The Psychology of Money

- Reading my post on The Power of Compounding

- Keeping up with my work on Instagram or Twitter

- Signing up for my mailing list below (on mobile) or the right side bar (on desktop)